It plays a crucial role in various industries, from retail to manufacturing, and helps businesses accurately track their stock movement and financial performance. However, LIFO may complicate financial reporting and obscure true profit margins, as the cost of goods sold might not accurately reflect the actual flow of inventory over time. Under the FIFO method, it’s assumed that the oldest inventory items are sold first, while the newest items remain in inventory. However, this does not necessarily represent the physical flow of goods; it’s an assumption to calculate cost of goods sold (COGS) and ending inventory. By reflecting lower inventory costs in COGS, FIFO can result in higher profits, improved financial statements, and potentially reduced tax liabilities.

How To Calculate LIFO

Compliance with one or both of the accounting practices facilitates easier auditing and financial analysis. FIFO’s widespread acceptance and straightforward logic mean it is supported by the majority of accounting and inventory management software. Mobile inventory management solutions like RFgen can automatically enforce FIFO rules in the warehouse. In inventory management, the FIFO (First-In, First-Out) method takes center stage, offering a performance of unmatched clarity and efficiency in the world of stock control. Imagine your inventory as a flowing river, where the oldest water—your earliest products—moves forward to be used first, ensuring nothing stagnates or loses its relevance. It is one of the most common methods to value inventory at the end of any accounting period; thus, it impacts the cost of goods sold during the particular period.

Other Valuation Methods

That means that you’ll use the oldest costs to calculate the cost of goods sold. A business in the trading of perishable items generally sells the items purchased first. The benefits of FIFO inventory method typically give the most accurate calculation of the inventory and sales profit. Other examples include retail businesses that sell foods or other products with an expiration date. No, because there are other inventory cost flow assumptions that might be a better fit for some businesses.

FIFO Inventory Method Explained

- But, what if you knew the cost of goods sold and wanted to calculate ending inventory instead?

- Keeping track of all incoming and outgoing inventory costs is key to accurate inventory valuation.

- Companies using perpetual inventory system prepare an inventory card to continuously track the quantity and dollar amount of inventory purchased, sold and in stock.

- By using older stock first, FIFO reduces the likelihood of inventory stagnation and minimizes holding costs.

- It’s required for certain jurisdictions, while others have the option to use FIFO or LIFO.

- Keep up with Michelle’s CPA career — and ultramarathoning endeavors — on LinkedIn.

Consistently review and refine your processes to adapt to changing business needs and market conditions. Second, every time a sale occurs, we need to assign the cost of units sold in the middle column. When a business buys identical inventory units for varying costs over a period of time, it needs to have a consistent basis for valuing the ending inventory and the cost of goods sold. As we discussed above, FIFO results in a higher gross profit during periods of rising prices. However, if a company used LIFO during a period of rising prices, gross profit would be lower.

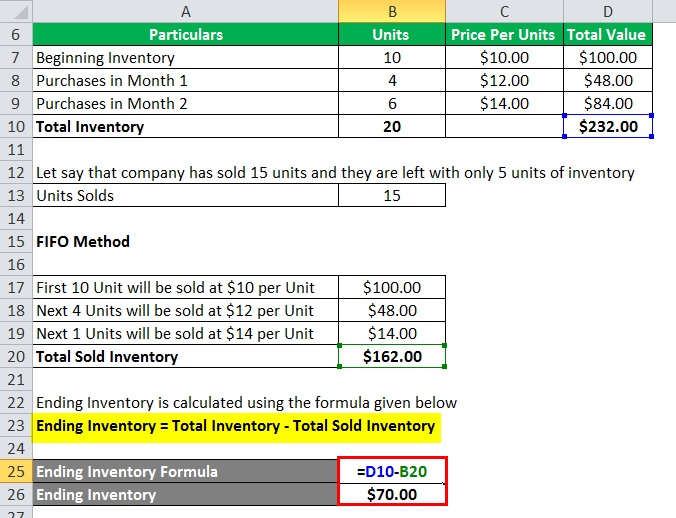

The company then applies first-in, first-out (FIFO) method to compute the cost of ending inventory. For example, if you sold 15 units, you would multiply that amount by the cost of your oldest inventory. However, if you only had 10 units of your oldest inventory in stock, you would multiply 10 units sold by the oldest inventory price, and the irs form 1040 remaining 5 units by the price of the next oldest inventory. Using the FIFO inventory method, this would give you your Cost of Goods Sold for those 15 units. While FIFO may lead to higher taxable income due to lower COGS in times of rising prices, in jurisdictions where tax implications are favorable, this can be a strategic advantage.

How Is the FIFO Method Calculated?

This results in inventory assets recorded at the most recent posts on the balance sheet. It is also the most accurate method of aligning the expected cost flow with the actual flow of goods which offers businesses a truer picture of inventory costs. First-in, first-out, also known as the FIFO inventory method, is one of four different ways to assign costs to ending inventory.

Let’s say on January 1st of the new year, Lee wants to calculate the cost of goods sold in the previous year. With the help of above inventory card, we can easily compute the cost of goods sold and ending inventory. With best-in-class fulfillment software and customizable solutions, we provide hassle-free logistics support to companies of all sizes. So, according to the periodic FIFO method, the COGS for the week is $140, and the ending inventory is $30. Before you put the games on your shelves, the market predicts they will sell quickly, so you order 50 more. Unfortunately, the cost has increased to $35 per game, so your inventory value for the next 50 is $1,750.

FIFO has several advantages, including being straightforward, intuitive, and reflects the real flow of inventory in most business practices. Many companies choose FIFO as their best practice because it’s regulatory-compliant across many jurisdictions. We’ll explore how the FIFO method works, as well as the advantages and disadvantages of using FIFO calculations for accounting.

The inventory balance at the end of the second day is understandably reduced by four units. On 1 January, Bill placed his first order to purchase 10 toasters from a wholesaler at the cost of $5 each. Under the FIFO Method, inventory acquired by the earliest purchase made by the business is assumed to be issued first to its customers. At the end of the year 2016, the company makes a physical measure of material and finds that 1,700 units of material is on hand. Not only does FIFO prevent materials from going unused or degrading, it also reduces waste and losses—not to mention storage costs. The construction and building materials industry benefits from FIFO as well.

This reduces the risk of inventory obsolescence, minimizes waste for perishable goods, and helps maintain consistency between your physical stock and accounting records. Cost of goods sold can be computed by using either periodic inventory formula method or earliest cost method. Although using the LIFO method will cut into his profit, it also means that Lee will get a tax break.

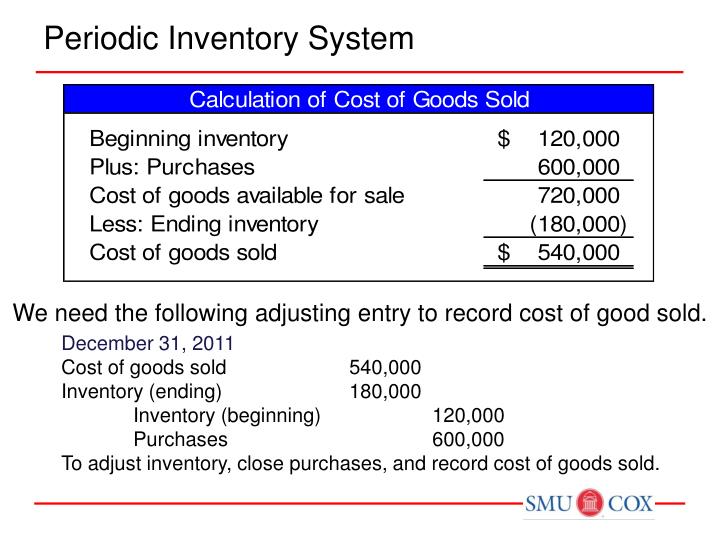

Every time a sale or purchase occurs, they are recorded in their respective ledger accounts. However, as we shall see in following sections, inventory is accounted for separately from purchases and sales through a single adjustment at the year end. Managers, accountants, and business owners benefit from mastering FIFO to optimize inventory systems and financial practices. To calculate the value of ending inventory using the FIFO periodic system, we first need to figure out how many inventory units are unsold at the end of the period. Here’s a summary of the purchases and sales from the first example, which we will use to calculate the ending inventory value using the FIFO periodic system. As we shall see in the following example, both periodic and perpetual inventory systems provide the same value of ending inventory under the FIFO method.